|

“Investment Planning” too often boils down to cookie-cutter investment mixes and overly simplified questionnaires regarding your financial needs. It’s better than nothing, but it’s impersonal and vague.

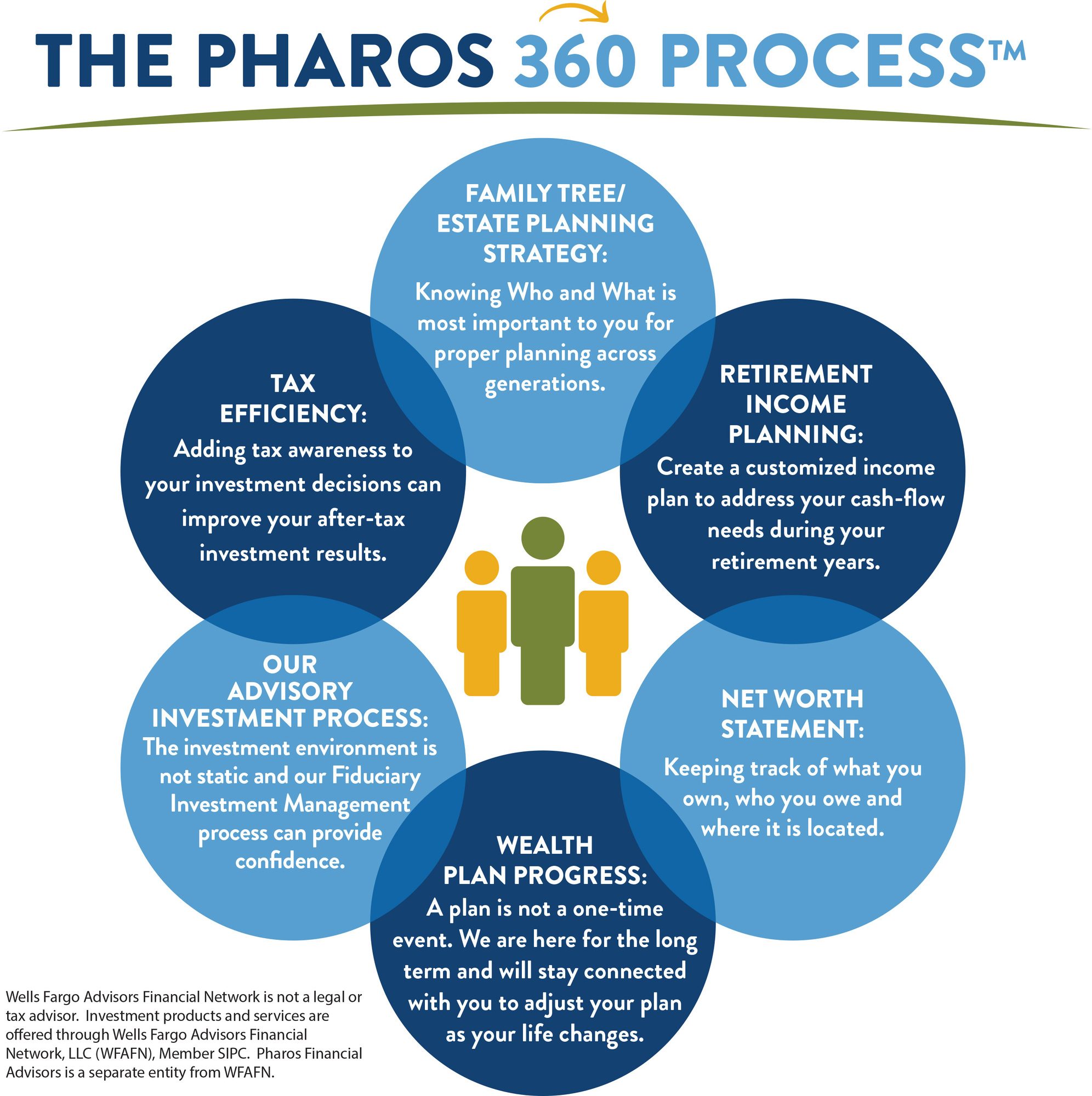

Wells Fargo Advisor's Envision® process offers us the technology needed to discuss your life expectations, create what-if scenarios, and offers complex modeling.

This interactive approach helps us to identify:

- Where you are now financially

- Where do you want to go

- How do you plan to get there

Once we have helped you explore your goals, together we’ll create an investment plan to support them.

The innovative Envision® planning process helps us keep you on track toward the future you’re planning. The process is flexible, so we can easily review and update your plan if your goals or circumstances change.

Best of all, it gives us the tools we need to:

- Decide on an appropriate investment strategy

- Review your progress

- Re-sync — or rethink — your approach, whenever necessary

- Life goals

- Education goals

- Assets

- Liabilities

- Cash-flow requirements

- Retirement planning needs

- Levels of acceptable investment risk

- Asset allocation objectives

It starts with a plan

Creating a plan can help you stay focused, plan for challenges ahead, and make choices that work for you.

The Envision planning process is the foundation we use to develop your retirement income plan. It can help you make choices and tackle the following topics:

- When and how can I retire with confidence?

- How can I help make my money last as long as I’m retired?

- Where will my income come from?

- How do I prepare for and respond to events throughout retirement?

- When and how should I address my legacy goals?

Part of your plan is how you spend your money – now and when you retire. Talk about it.

Common risks to address

While we develop your retirement plan, you’ll want to look at impacting events such as inflation, market conditions, health needs, and how long you’re likely to live. Understanding the impact these challenges may have on your savings and planning a withdrawal strategy can help you stay the course.Have an ongoing process

Planning for retirement is not a “one and done” kind of activity. A good plan should be checked regularly and adjusted, as necessary. We will keep an eye on your portfolio, talk about your expectations, and help you prepare for the unexpected.Schedule an annual checkup with us to review your plans, your current circumstances, and your portfolio. We’ll work together to discuss your choices and what works for you.

Next steps

- Think about what you hope your retirement will be.

- Write down all your possible sources of income and expenses in retirement.

- Take a look at your portfolio and call us if you have any questions about changing your asset allocation.

- Call us to start on your personalized retirement income plan.

By engaging us as your Fiduciary Portfolio Manager (through an advisory relationship), you can be assured that your interests are always placed first. Fiduciary Portfolio Management services are provided on a fee basis; commissions are not charged. This helps ensure our interests are aligned with yours. Our fee schedule is competitive and cost effective to you.

We recognize that your needs are unique, ever changing, and that you require more from your financial institution. Effectively managing wealth involves more than just off-the-shelf services. It requires specialized experience, deep industry knowledge, and precisely crafted solutions. You can expect an elevated experience delivered through personalized service, tailored solutions, and the specialization of a boutique practice, backed by the strength and resources of one of the largest global financial institutions.

We can discuss the programs with you and see what fits your situation – and what makes you feel more confident in helping you reach your goals.

Decide if you would like some extra help with making your investment decisions.

Make an appointment to talk with us about advisory accounts.

We recognize that your needs are unique, ever changing, and that you require more from your financial institution. Effectively managing wealth involves more than just off-the-shelf services. It requires specialized experience, deep industry knowledge, and precisely crafted solutions. You can expect an elevated experience delivered through personalized service, tailored solutions, and the specialization of a boutique practice, backed by the strength and resources of one of the largest global financial institutions.

Flexible range of alternatives

You can choose which advisory services program to implement. We offer an array of programs. You can decide what products you would like to have managed, such as mutual funds, exchange-traded funds (ETFs), stocks, bonds, and commodity-based investments.We can discuss the programs with you and see what fits your situation – and what makes you feel more confident in helping you reach your goals.

Next steps

Decide if you would like some extra help with making your investment decisions.

Make an appointment to talk with us about advisory accounts.

The fees for advisory programs are asset-based and assessed quarterly in advance. There may be a minimum fee to maintain this type of account. Fees include advisory services, performance measurement, transaction costs, custody services, and trading. These fees do not cover the fees and expenses of any underlying exchange traded fund (ETF), closed-end funds, or mutual funds in the portfolio. Advisory accounts are not designed for excessively traded or inactive accounts and are not appropriate for all investors. Please carefully review the Wells Fargo Advisors advisory disclosure document for a full description of our services, including fees and expenses. The minimum account size for these programs is between $10,000 and $2,000,000.

- Everyone could use an estate plan – not just the wealthy.

- 5 documents are essential for many estate plans.

- An estate planning attorney and your accountant will work with your Financial Advisor.

Estate planning: a matter of control

You might associate estate planning with famous people you see in the news. In fact, estate planning could be appropriate for everyone.Consider your assets: bank accounts, investment accounts, 401(k) or 403(b) plan accounts, house, cars, jewelry, and heirlooms. This is your estate and your estate plan can define what you would like to happen to these assets when you die.

An estate plan can also take care of you as you get older or if you become ill or incapacitated. Being wealthy has little to do with it.

If you don’t make your own plan, your family may be left scrambling at an already difficult time. Bottom line: If you don’t decide, someone will decide for you.

Five essential documents

These five documents are often essential to an estate plan:- Will - Instructions for distributing your assets when you die. You will name a personal representative (executor) to pay final expenses and taxes and distribute remaining assets. Name a guardian to raise your minor children if both parents die.

- Durable power of attorney – You give a trusted individual management power over your assets if you can’t manage them yourself. This document is effective only while you’re alive.

- Health care power of attorney - You choose someone to make medical decisions on your behalf if something were to happen and you can’t make them yourself.

- Living will – Shares your intentions about life-sustaining medical measures if you are terminally ill. No one is given authority to speak for you.

- Revocable living trust - You can provide for continued management of your financial matters while you are alive, after your death, and even for generations after.

Why beneficiary designations are important

Beneficiary designations can be an easy way to transfer an account or insurance policy when you die. But if you didn’t complete beneficiary designations, or haven’t updated them, they can cause issues with your estate plan.Designations on forms are often filled out without much thought – but they’re important and deserve your attention. Beneficiary designations on forms like your insurance policy and 401(k) take priority over other estate planning documents, like your will or trust.

Let’s say you specify in your will you want everything to go to your spouse after your death. But you never changed the beneficiary designation on your life insurance policy and it names your ex-spouse. Your ex may end up getting the proceeds.

Turn to a team of professionals

Making the decisions involved with estate planning may seem overwhelming. It doesn’t have to be. You can start by organizing your important documents.Turn to a team of trusted professionals, including your financial advisor, an estate planning attorney, and your accountant. They know the questions to ask and can help you avoid potential pitfalls.

If you currently don’t have relationships with an attorney and an accountant, we can make some recommendations. We can also discuss our role in the planning process and how you can get started.

Next steps

- Make an appointment with us to talk about your estate planning goals.

- Start gathering your financial documents.

- Check the beneficiary designations on your financial and investment accounts.

Trust services available through banking and trust affiliates in addition to non-affiliated companies of Wells Fargo Advisors.

Wells Fargo Advisors and its affiliate do not provide tax or legal advice. Please consult with your tax and/or legal advisors before taking any action that may have tax and/or legal consequences. Any estate plan should be reviewed by an attorney who specializes in estate planning and is licensed to practice law in your state.

- Generally you have four distribution choices for your qualified employer–sponsored retirement plan (QRP) assets

- Each has unique factors to keep in mind

- Know all of your options before making a decision

Decide which option is right for you

If you’re changing jobs or retiring, you’ll need to decide what to do with assets in your 401(k) or other qualified employer-sponsored retirement plan (QRP). These savings can represent a significant portion of your retirement income, so it’s important you carefully evaluate all of the options.Generally, you have four options:

- Roll the assets to an Individual Retirement Account (IRA)

- Leave the funds in your former employer’s retirement plan (if allowed)

- Move savings to your new employer’s plan (if allowed)

- Withdraw or “distribute” the money

Roll the assets to an IRA

Rolling your retirement savings to an IRA provides the following features:- Assets continue their tax-advantaged status and growth potential

- You can continue to make annual contributions, if eligible

- An IRA often gives you more investment options than are typically available in an employer’s plan

- You also may have access to investment advice

Before rolling your assets to an IRA consider the following:

- IRA fees and expenses are generally higher than those in your employer’s retirement plan

- Loans from an IRA are prohibited

- In addition to ordinary income taxes, distributions prior to age 59 1/2 may be subject to a 10% IRS tax penalty

- IRAs are subject to state creditor laws

- If you own appreciated employer securities, favorable tax treatment of the net unrealized appreciation (NUA) is lost if rolled into an IRA

Leave the funds with your former employer

You may be able to leave your retirement plan savings in your former employer’s plan, assuming the plan allows and you are satisfied with the investment options. You will continue to be subject to the plan’s rules regarding investment choices, distribution options, and loan availability.Keeping assets in the plan features:

- Investments keep their tax-advantaged growth potential

- You retain the ability to leave your savings in their current investments

- You may avoid the 10% IRS early distribution penalty on withdrawals from the plan if you leave the company in the year you turn 55 or older (age 50 or older for certain public safety employees)

- Generally, have bankruptcy and creditor protection

- Favorable tax treatment may be available for appreciated employer securities owned in the plan

Move savings to your new employer’s plan

If you’re joining a new company, moving your retirement savings to your new employer’s plan may make sense. This may be appropriate if:- You want to keep your retirement savings in one account

- You’re satisfied with the investment choices offered by your new employer’s plan

Withdraw or “distribute” the money

Carefully consider all of the financial consequences before cashing out. The impact will vary depending on your age and tax situation. Distributions prior to age 59 1/2 may be subject to both ordinary income taxes and a 10% IRS tax penalty. If you must access the money, consider withdrawing only what you need until you can find other sources of cash.Features

- You have immediate access to your retirement savings and can use however you wish.

- Although distributions from the plan are subject to ordinary income taxes, penalty-free distributions can be taken if you turn:

- Age 55 or older in the year you leave your company.

- Age 50 or older in the year you stop working as a public safety employee (certain local, state or federal) — such as a police officer, firefighter, emergency medical technician, or air traffic controller — and are taking distributions from a governmental defined benefit pension or governmental defined contribution plan. Check with the plan administrator to see if you are eligible.

- If you own employer securities, a distribution may qualify for the favorable tax treatment of NUA.

- Your former employer is required to withhold 20% of your distribution for federal taxes.

- Distribution may be subject to federal, state and local taxes unless rolled over to an IRA or another employer plan within 60 days.

- Your investments lose their tax-advantaged growth potential.

- Your retirement may be delayed, or the amount you’ll have to live on later may be reduced.

- Depending on your financial situation, you may be able to access a portion of your funds while keeping the remainder saved in a retirement account. This can help lower your tax liability while continuing to help you save for your retirement. Ask your plan administrator if partial distributions are allowed.

- If you leave your company before the year you turn 55 (or age 50 for public service employees), you may owe a 10% IRS tax penalty on the distribution.

What to consider if you own company stock

Net unrealized appreciation (NUA) is defined as the difference between the value at distribution of the employer security in your plan and the stock’s cost basis. The cost basis is the original purchase price paid within the plan. Assuming the security has increased in value, the difference is NUA. NUA of employer securities received as part of an eligible lump-sum distribution from an employer retirement plan qualifies for special tax treatment. In most cases, NUA will be available only for lump-sum distributions — partial distributions do not qualify.We can help educate you so you can decide which option makes the most sense for your specific situation.

Next steps

- Learn about your choices before taking a distribution

- Pay special attention to taxes, penalties and fees associated with each action

- Contact us or your tax professional if you have questions about how to proceed

When considering rolling over assets from an employer plan to an IRA, factors that should be considered and compared between the employer plan and the IRA include fees and expenses, services offered, investment options, when penalty free distributions are available, treatment of employer stock, when required minimum distributions begin, protection of assets from creditors, and bankruptcy. Investing and maintaining assets in an IRA will generally involve higher costs than those associated with employer-sponsored retirement plans. You should consult with the plan administrator and a professional tax advisor before making any decisions regarding your retirement assets. Withdrawals are subject to ordinary income tax and may be subject to a federal 10% penalty if taken prior to age 59 1/2.

Wells Fargo Advisors does not provide tax or legal advice. Please consult with your tax and legal advisors to determine how this information may impact your own situation.